The segmental analysis is based on the information disclosed in the notes to the accounts in each syndicate’s financial statements. The data has been curated by ICMR and is available as part of the ICMR.Data offering.

Although this section will focus on the aggregated data for four lines (Reinsurance, Casualty, Property and Specialty) the underlying data is more granular. All lines with the exception of Accident & Health have a higher number of syndicates participating in 2023 versus 2015, while those dipping and then increasing perhaps indicate where the most marked remediation and recovery activity has taken place.

5.1 Number of syndicates reporting by COB

COB

2015

2016

2017

2018

2019

2020

2021

2022

2023

Accident and health

50

50

47

45

46

48

54

52

50

Energy

25

25

26

30

29

34

34

35

34

MAT

82

84

78

80

78

79

96

96

100

Motor

48

49

47

47

49

52

50

56

54

Pecuniary loss

66

66

63

61

64

66

74

71

73

Property

71

73

69

70

66

69

80

83

84

Reinsurance

74

76

71

72

71

74

87

88

93

Third party liability

69

69

62

65

62

64

74

78

82

Table 5.1: Number of syndicates that reported gross underwriting performance data by class of business over the period, including run-offs

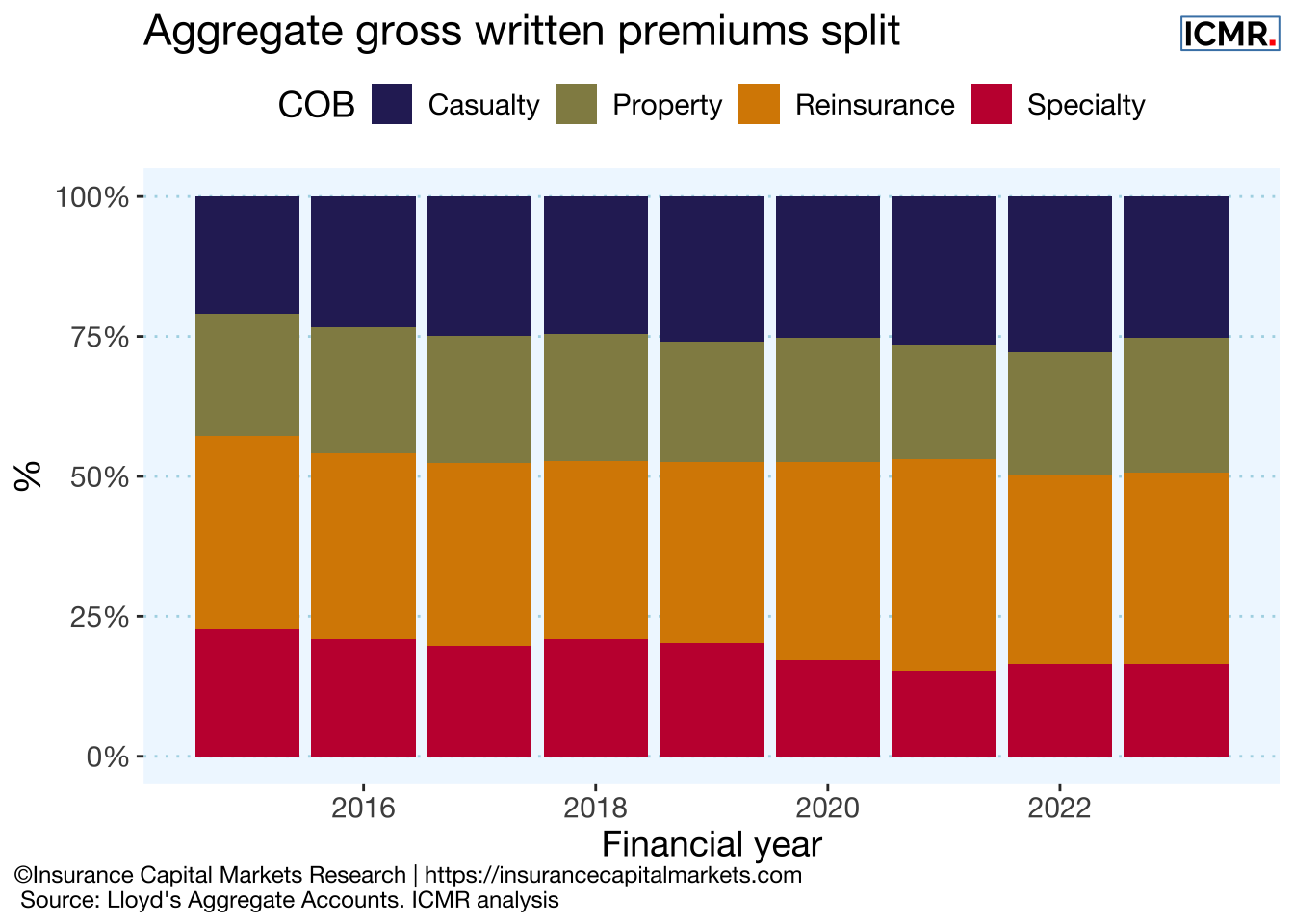

5.2 Aggregate gross written premium by COB

Aggregating the data to only four classes shows that the traditional specialty lines have become less material for Lloyd’s over time, while new classes such as Cyber have grown significantly as part of Casualty.

Figure 5.1: Gross written premium split by class of business

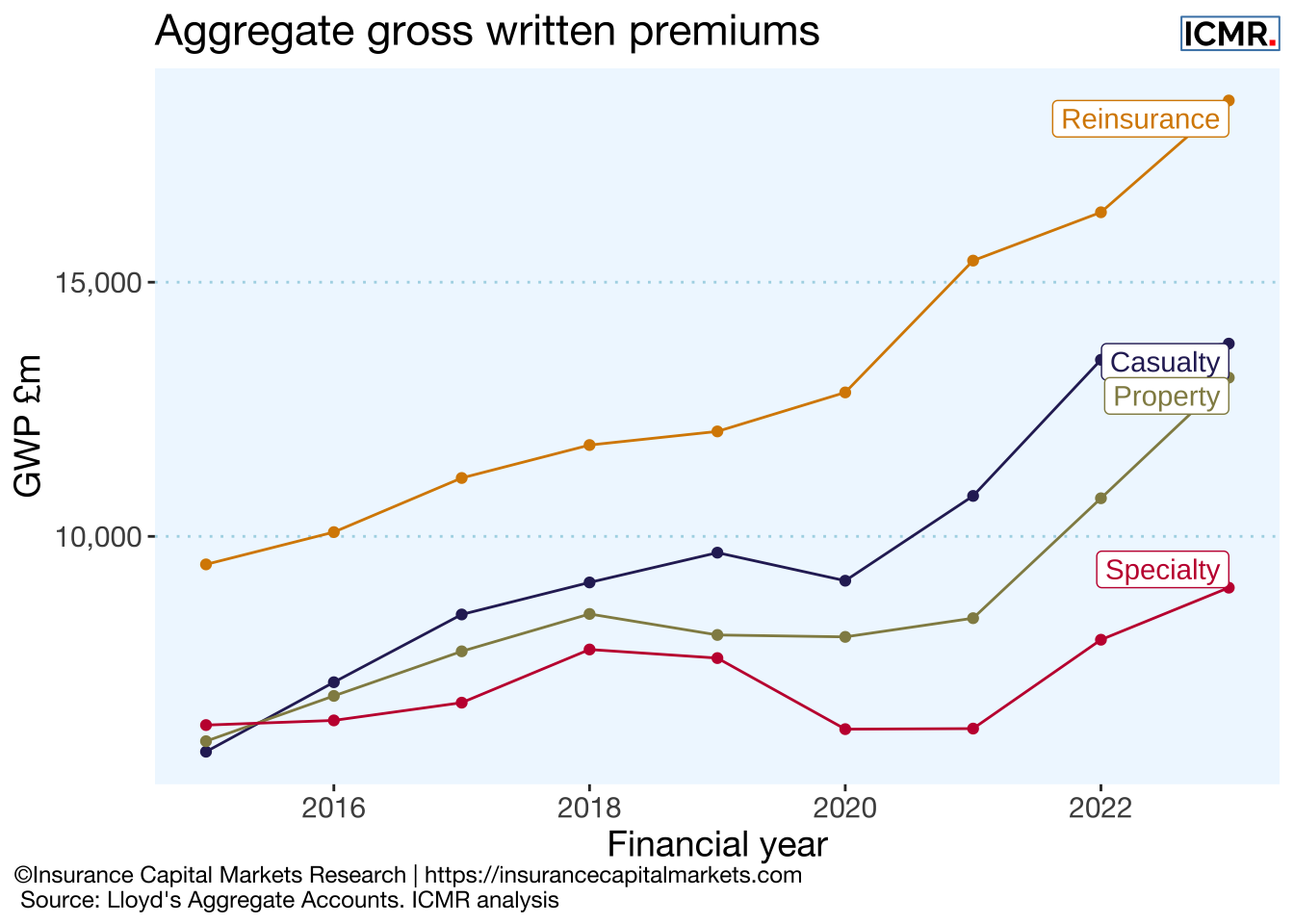

The strongest percentage growth has been in Casualty. Although Reinsurance remains the largest single class, it has reduced as a proportion of the whole. The Specialty class is now the smallest major class in the market.

Figure 5.2: Lloyd’s aggregate gross written premium

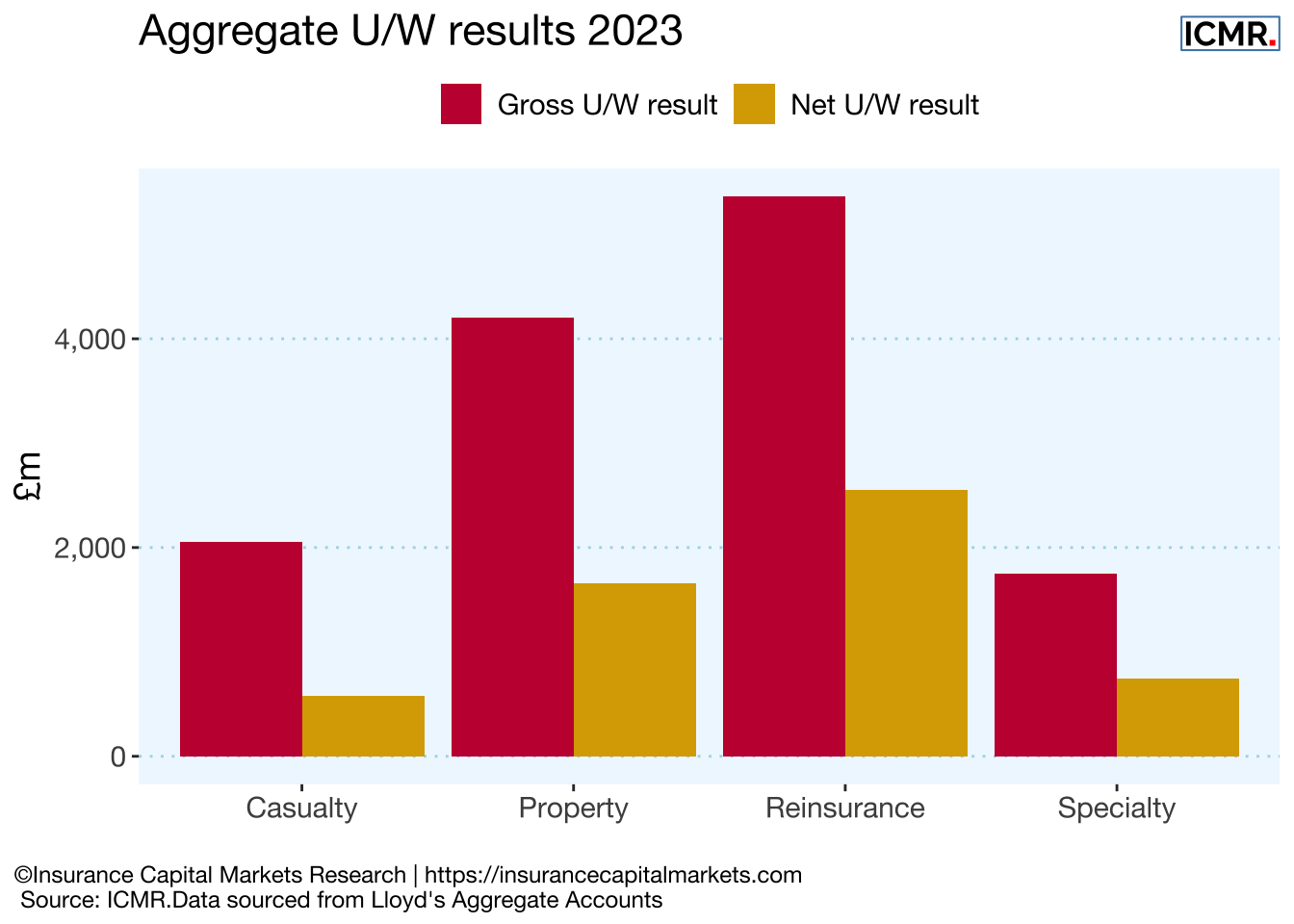

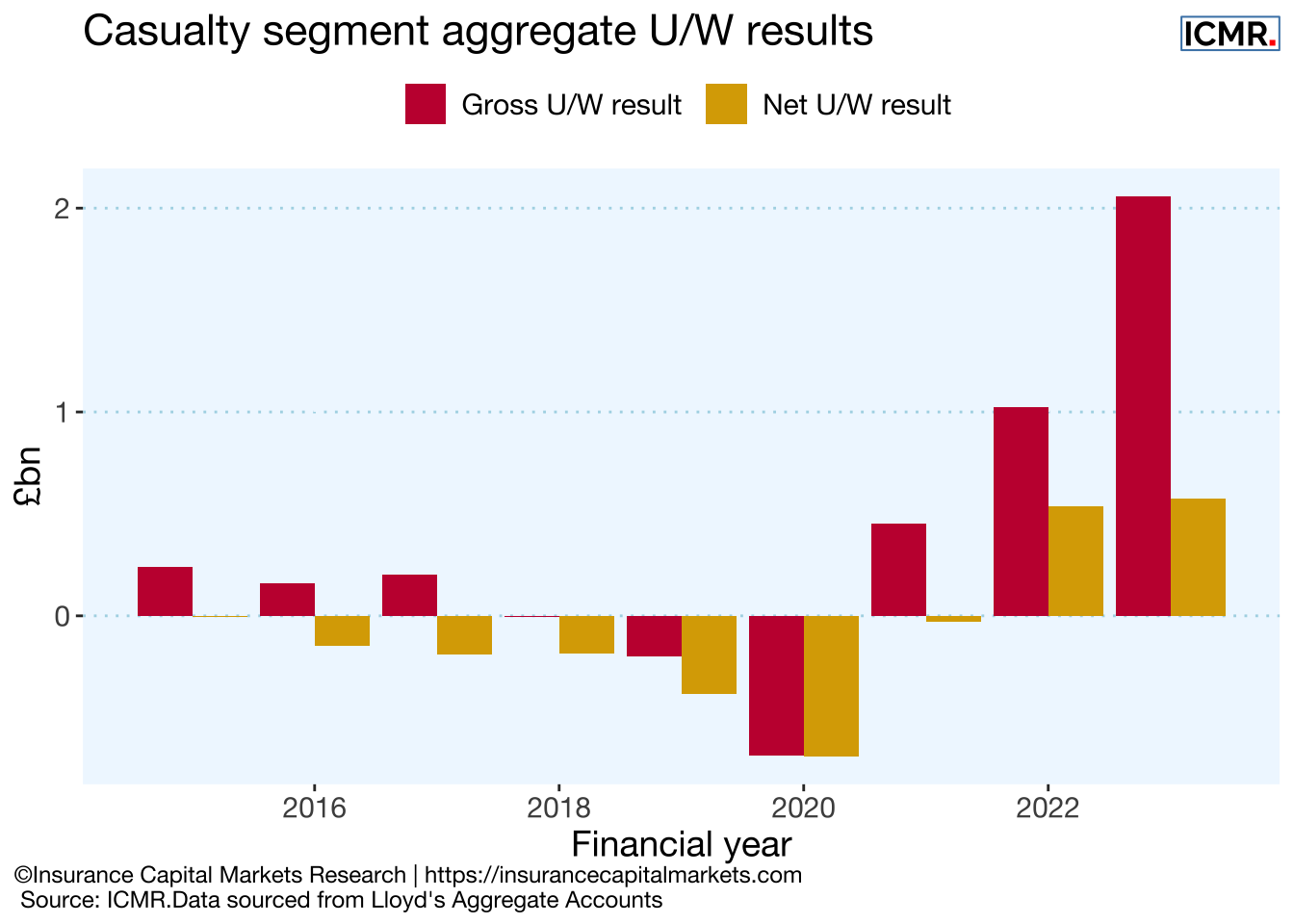

5.3 Aggregate underwriting results by COB

In 2023, all four classes delivered gross and net underwriting profits in the aggregate.

Figure 5.3: Aggregate gross and net underwriting results at Lloyd’s in 2023

The next sections delve deeper into the data by COB, reviewing the performance over time, the gross U/W risk vs reward profile and changes in market concentration.

Reviewing performance on a gross performance basis has the advantage of eliminating the impact of different reinsurance structures, particularly inter-group reinsurance and legacy transactions.

All classes show a reduction in the operating expense ratio over time, and all classes but Casualty also show a reduction in market share of the top 5 biggest syndicates by GWP.

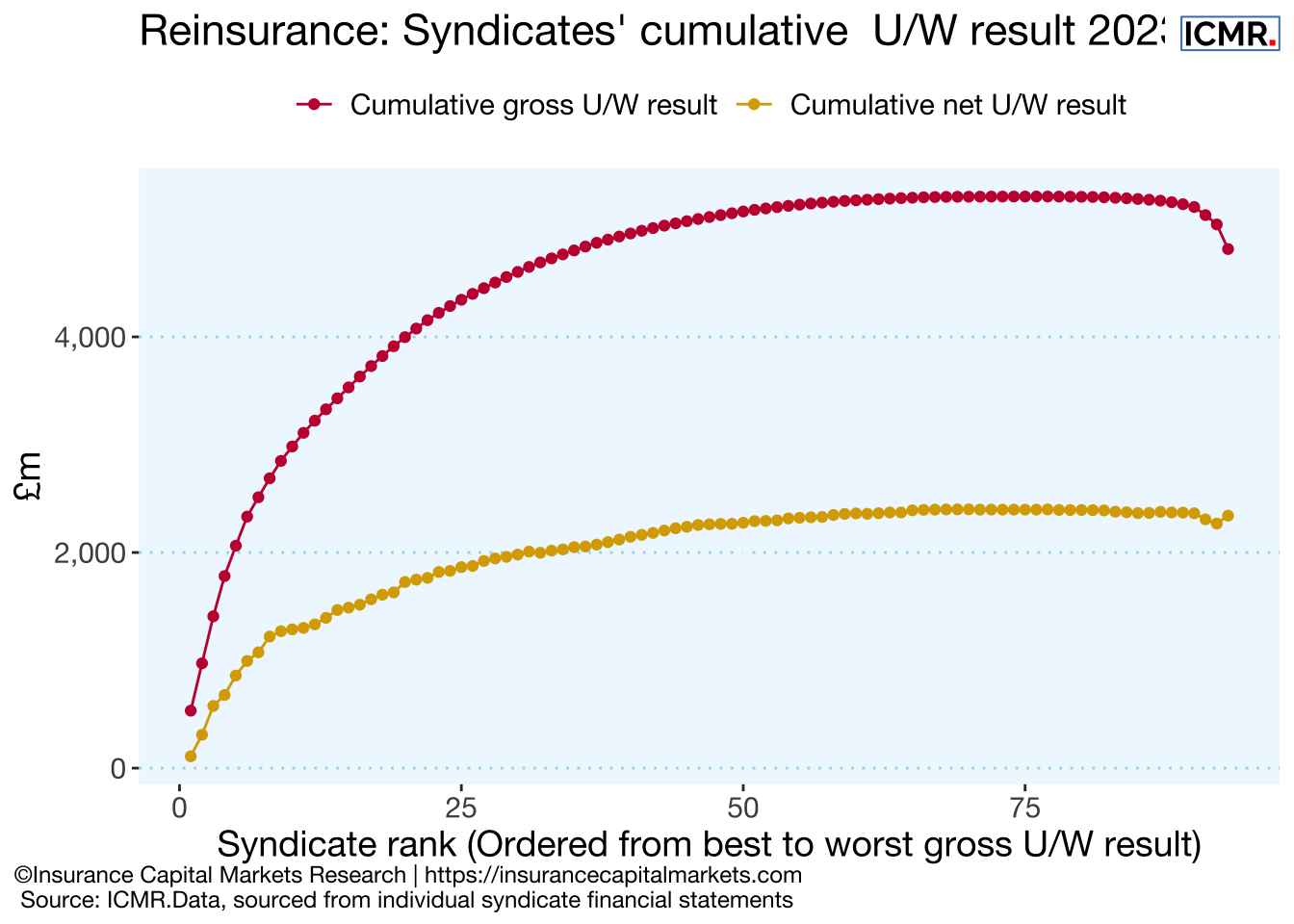

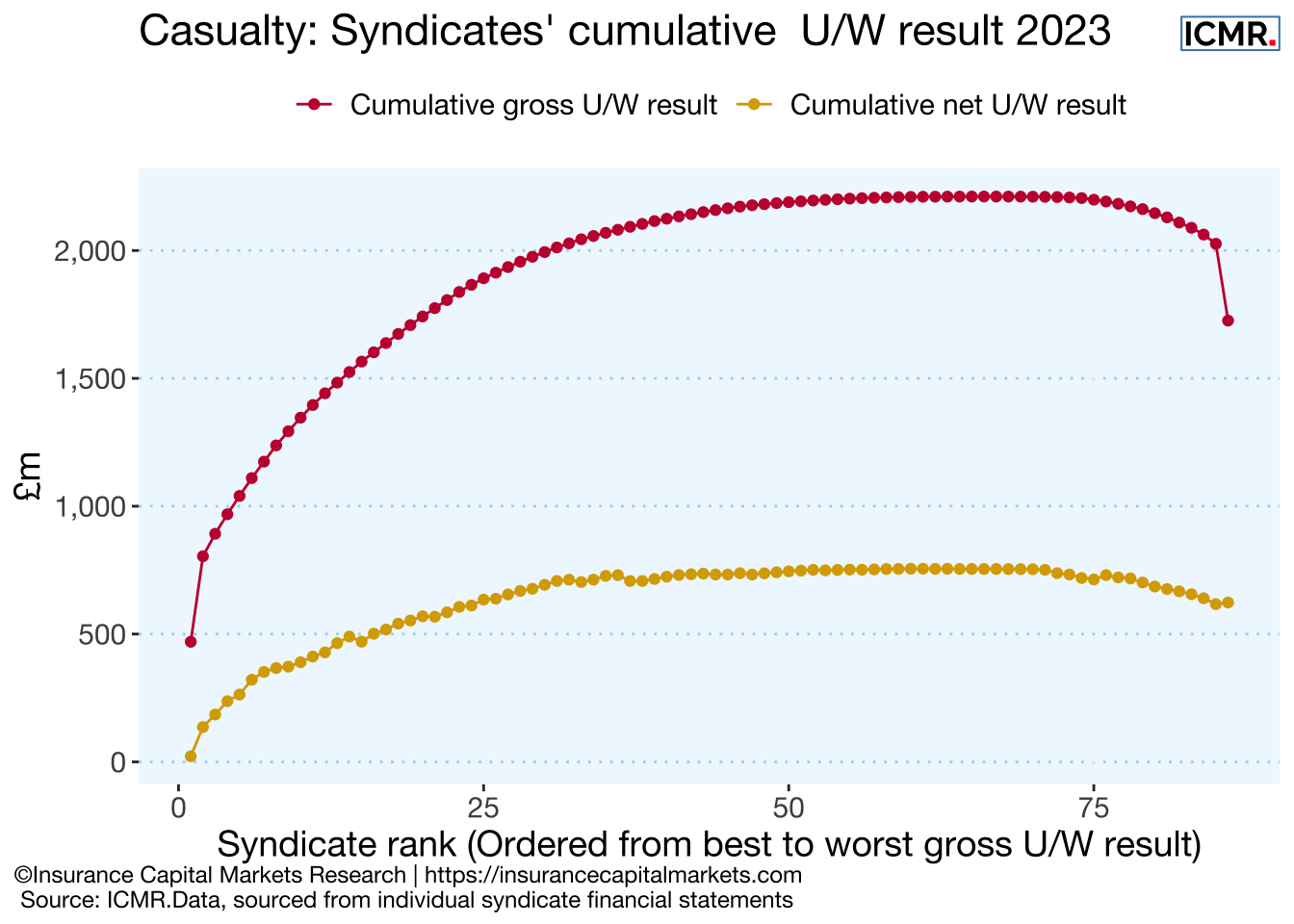

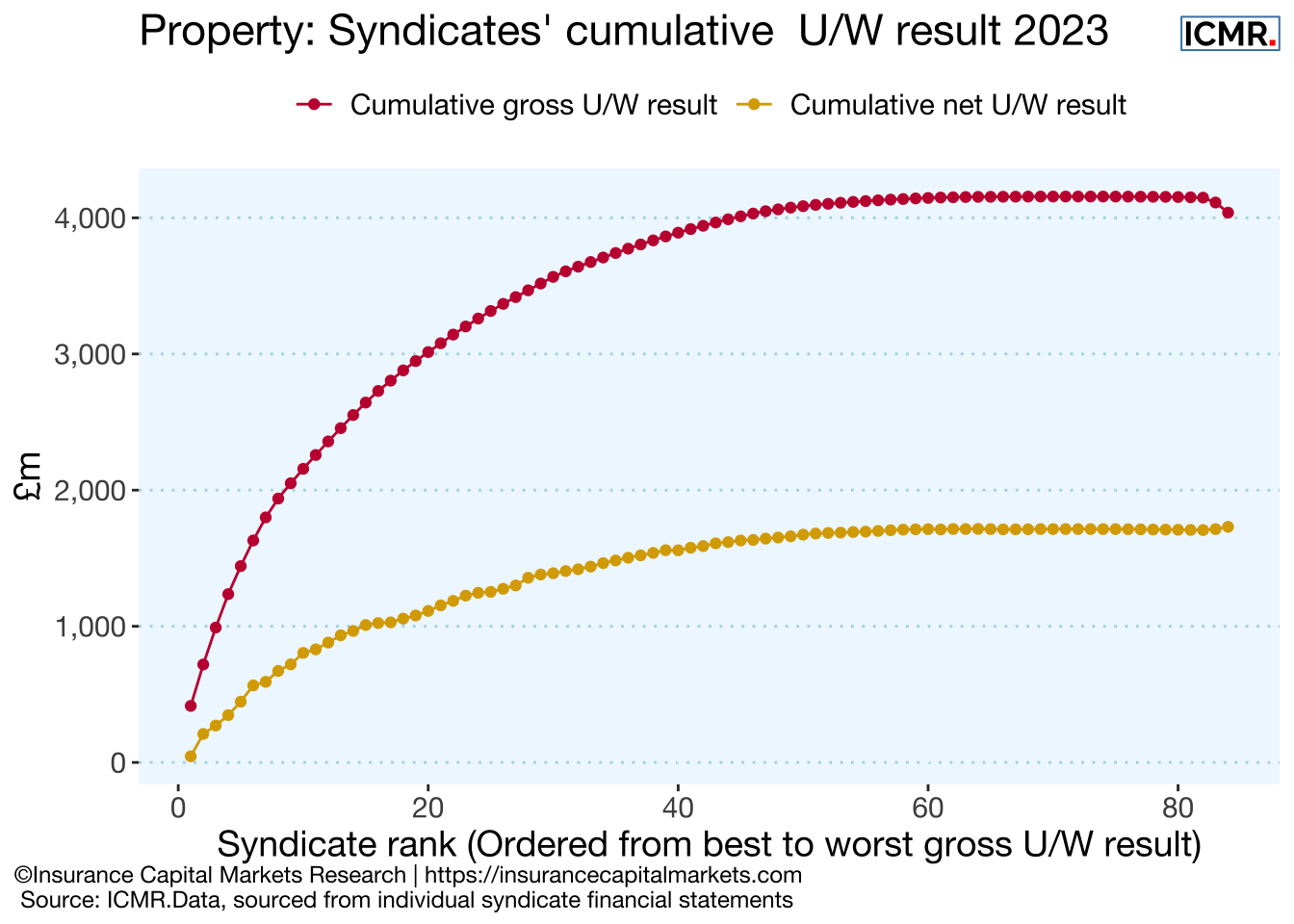

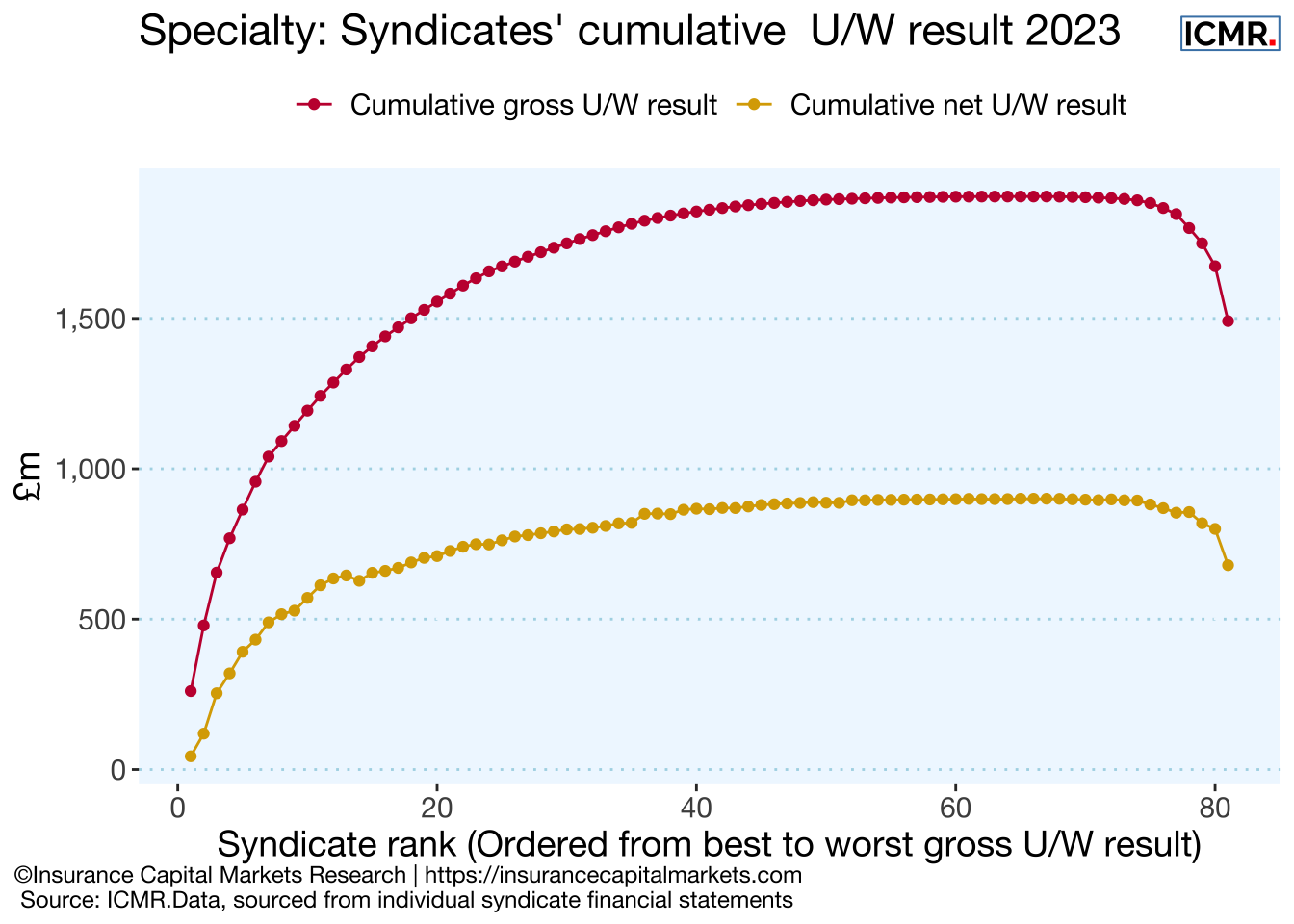

Figure 5.4: Cumulative syndicate gross and net underwriting results, ordered from most to least profitable on a gross basis. The net underwriting results follow the gross in the same syndicate order. The difference in quantum between the lines is reinsurers’ share of the gross profit. SPAs have been excluded.

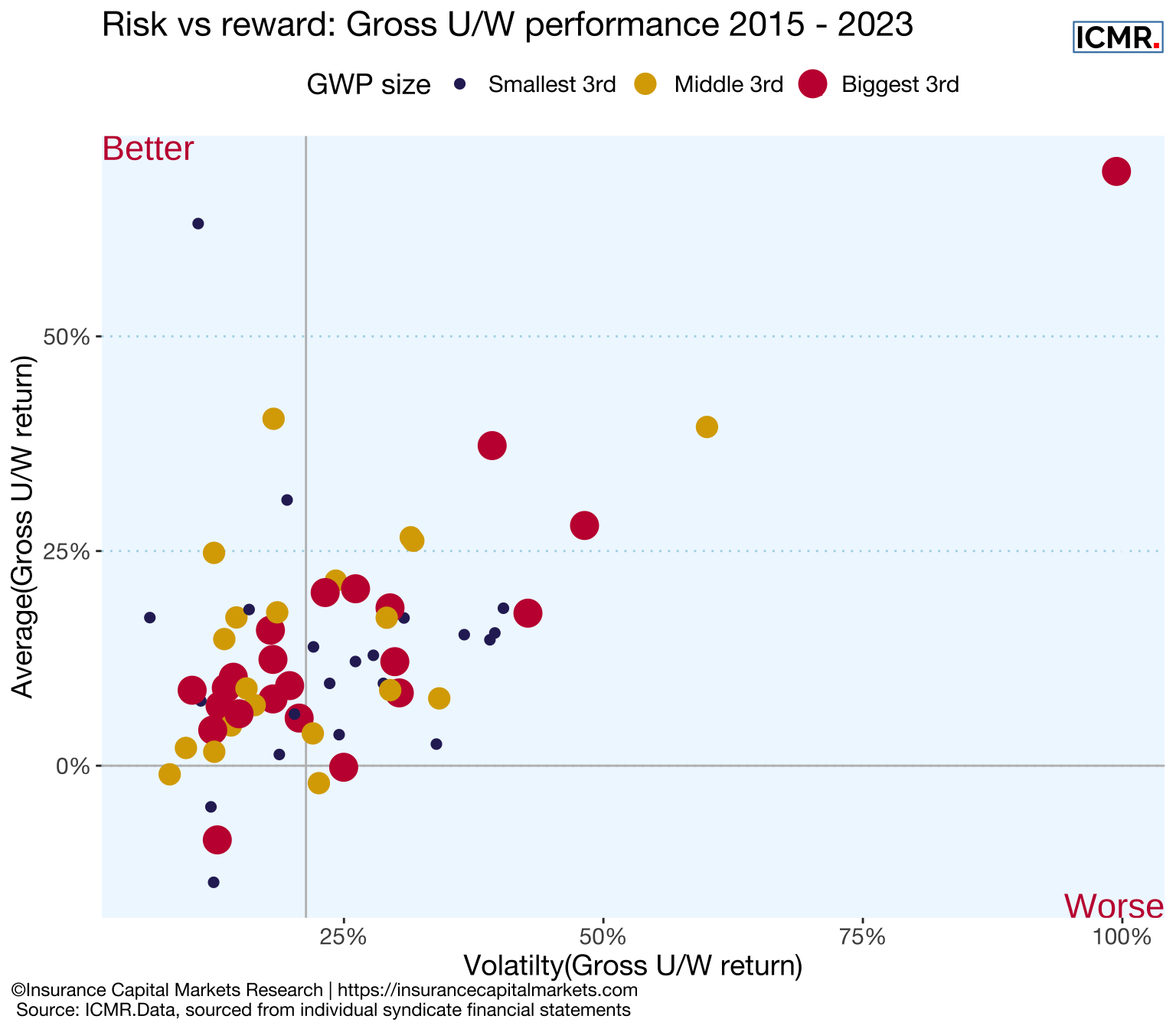

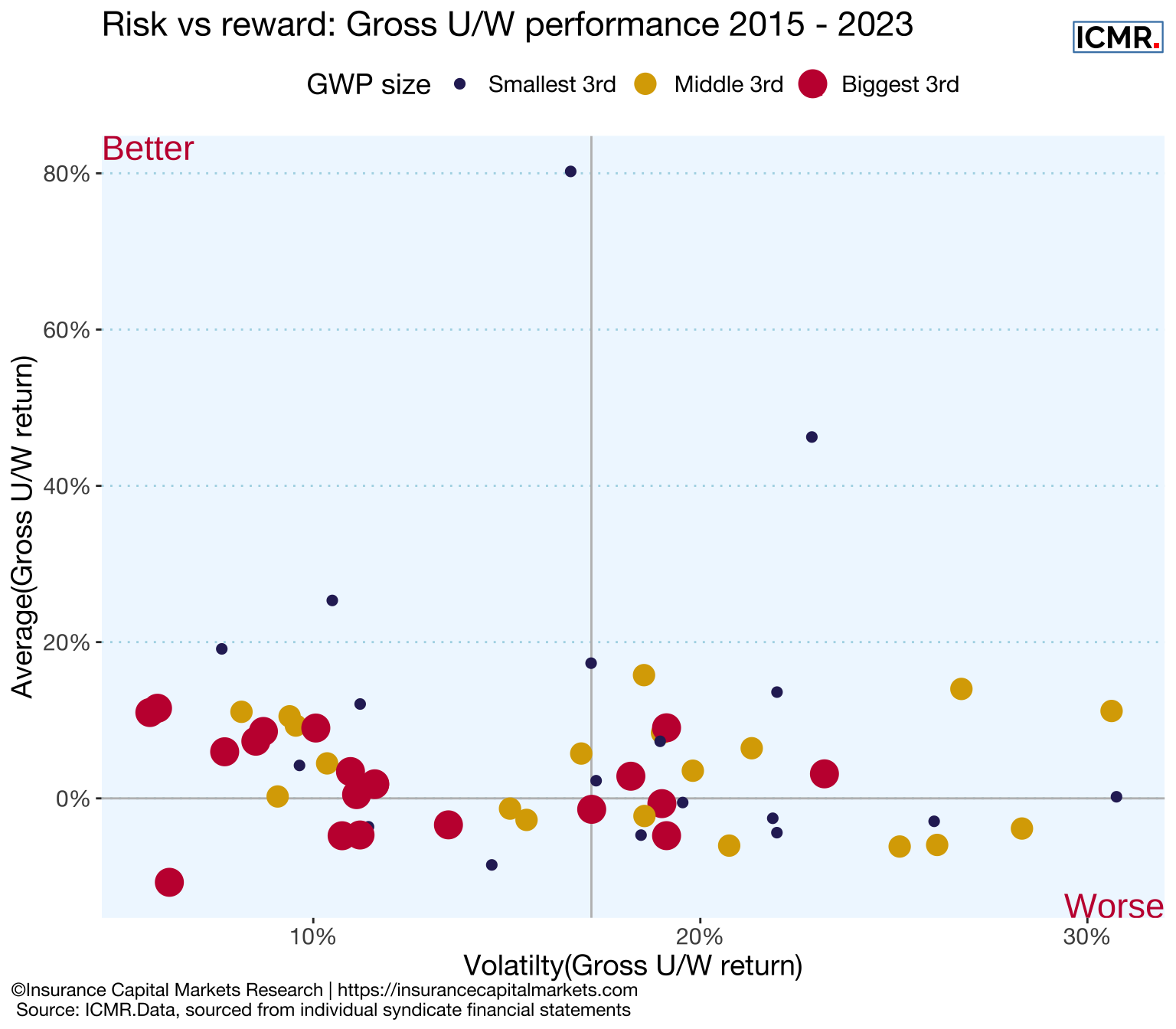

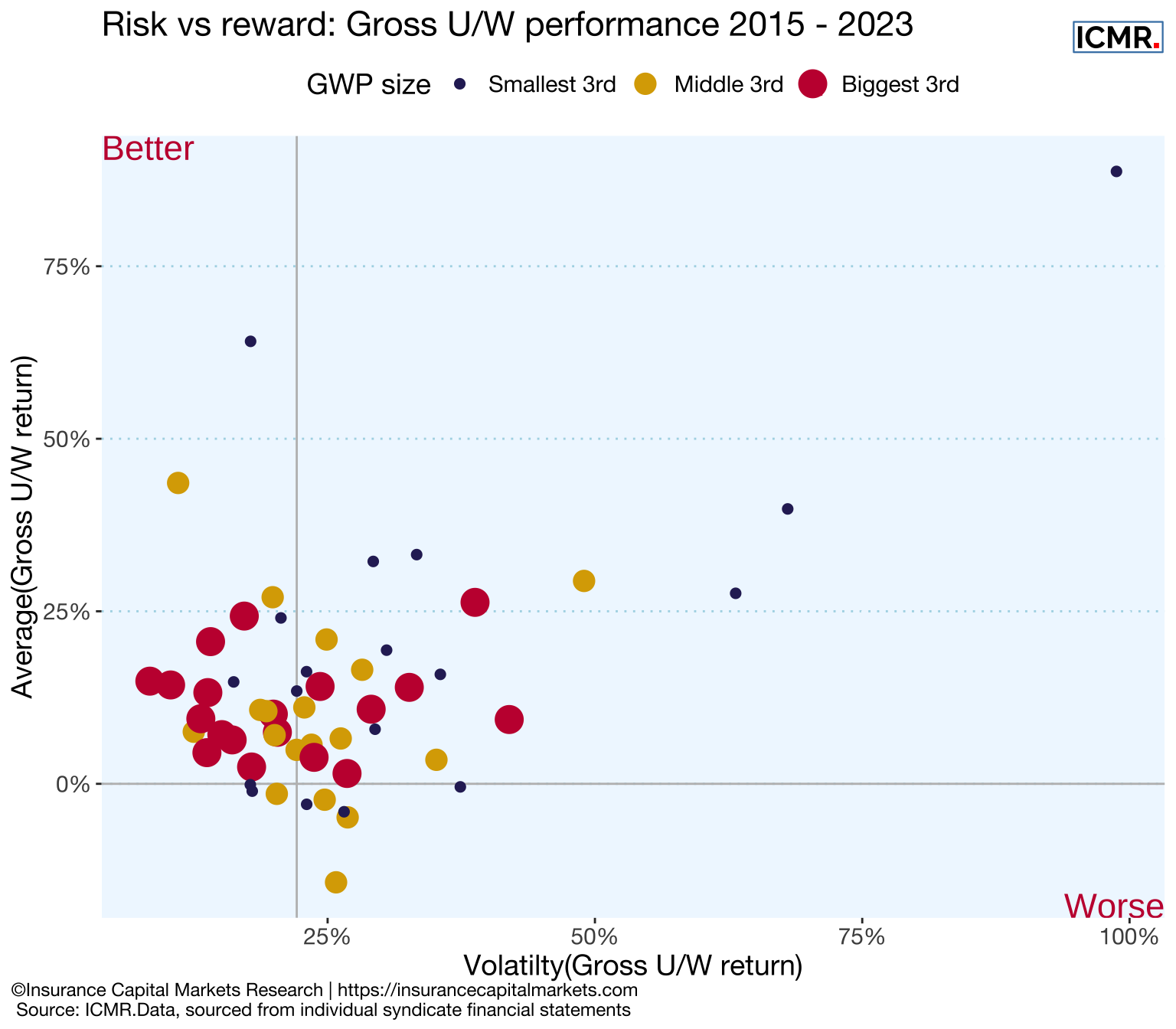

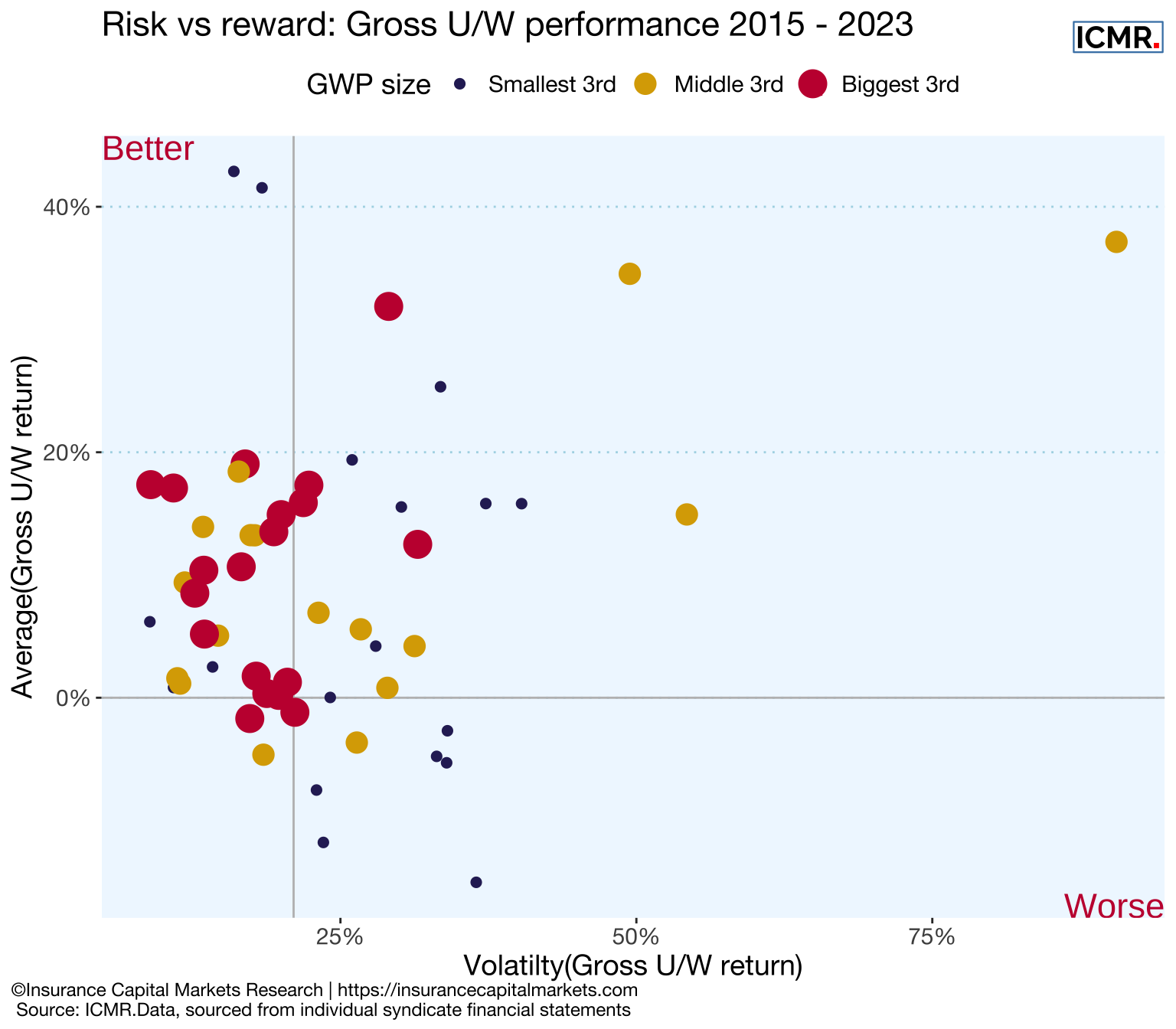

Figure 5.5: Distribution of syndicates’ annual gross U/W return (= 100% - Gross combined ratio) over time. Syndicates (dots) in the top left represent entities with high gross U/W returns and low volatility (good), syndicates (dots) in the bottom right have more volatile and lower gross U/W returns (bad). The vertical line represents the median.

Table 5.2: GWP, gross & net U/W result from Lloyd’s Aggregate Accounts, number of syndicates and top 5 share from individual non-life syndicate financial statements. Source: ICMR.Data

Financial year

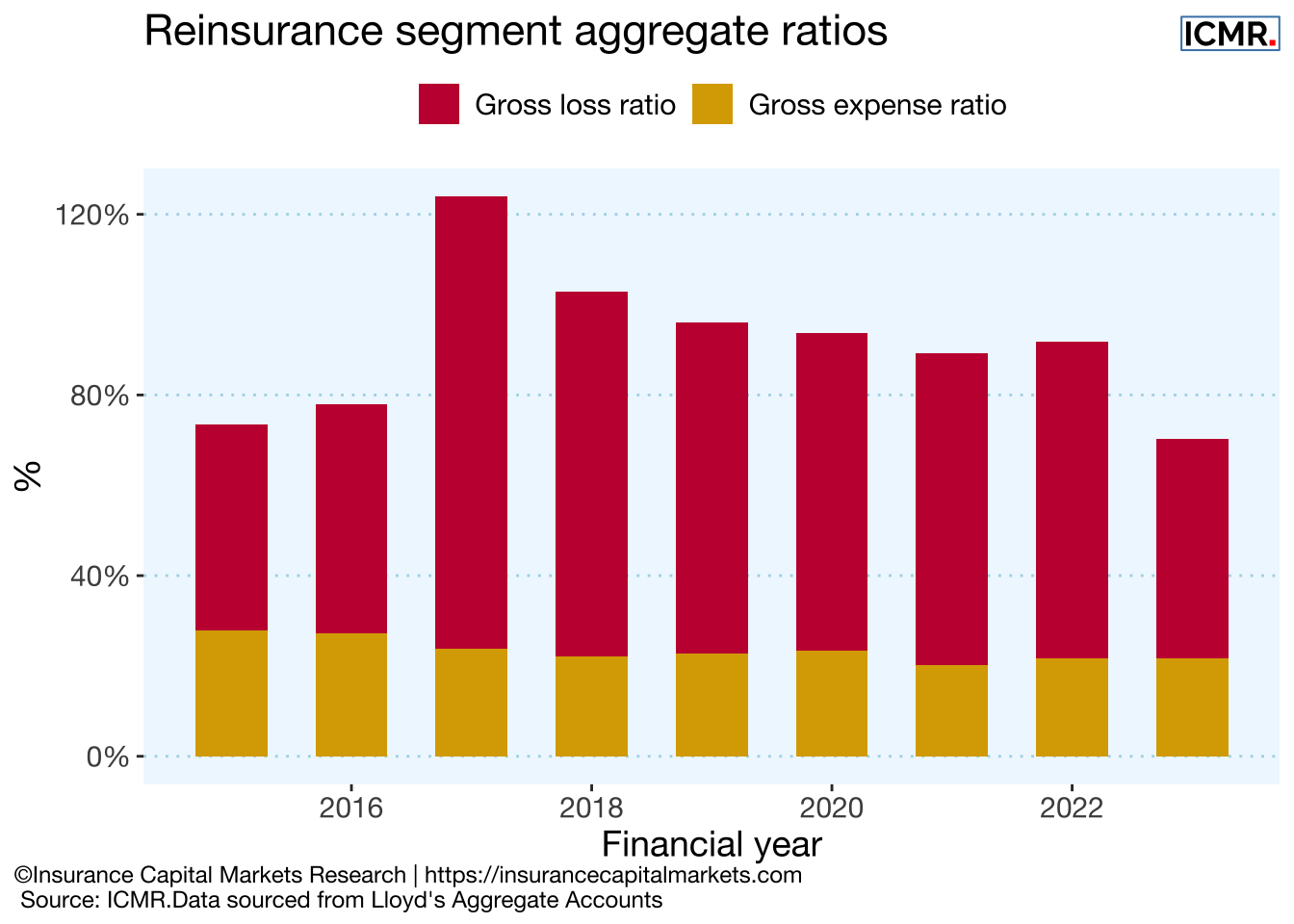

Gross loss ratio

Gross expense ratio

Gross combined ratio

2015

45.8%

27.8%

73.5%

2016

50.8%

27.3%

78.1%

2017

100.2%

23.8%

123.9%

2018

80.9%

22.1%

102.9%

2019

73.3%

22.7%

96.1%

2020

70.3%

23.5%

93.7%

2021

69.2%

20.1%

89.3%

2022

70.0%

21.7%

91.7%

2023

48.5%

21.7%

70.2%

Mean

67.7%

23.4%

91.1%

StDev

17.4%

2.6%

16.5%

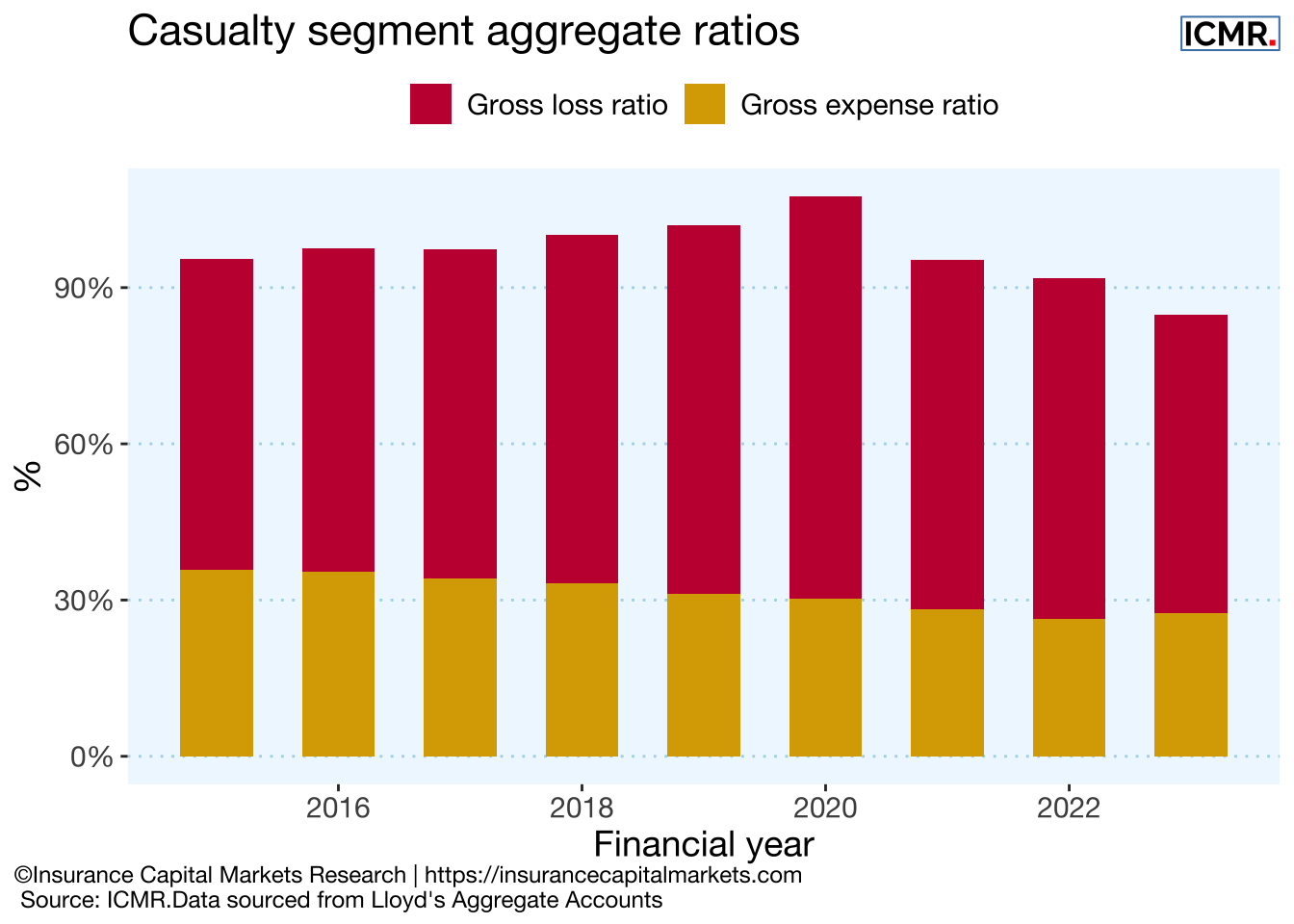

Table 5.3: ICMR.Data, sourced from Lloyd’s Aggregate Accounts

Figure 5.8: Cumulative syndicate gross and net underwriting results, ordered from most to least profitable on a gross basis. The net underwriting results follow the gross in the same syndicate order. The difference in quantum between the lines is reinsurers’ share of the gross profit. SPAs have been excluded.

Figure 5.9: Distribution of syndicates’ annual gross U/W return (= 100% - Gross combined ratio) over time. Syndicates (dots) in the top left represent entities with high gross U/W returns and low volatility (good), syndicates (dots) in the bottom right have more volatile and lower gross U/W returns (bad). The vertical line represents the median.

Table 5.4: GWP, gross & net U/W result from Lloyd’s Aggregate Accounts, number of syndicates and top 5 share from individual non-life syndicate financial statements. Source: ICMR.Data

Financial year

Gross loss ratio

Gross expense ratio

Gross combined ratio

2015

59.8%

35.7%

95.6%

2016

62.1%

35.5%

97.6%

2017

63.3%

34.1%

97.4%

2018

66.8%

33.3%

100.0%

2019

70.9%

31.2%

102.1%

2020

77.3%

30.2%

107.5%

2021

67.1%

28.3%

95.4%

2022

65.4%

26.4%

91.8%

2023

57.2%

27.5%

84.7%

Mean

65.5%

31.4%

96.9%

StDev

6.0%

3.5%

6.4%

Table 5.5: ICMR.Data, sourced from Lloyd’s Aggregate Accounts

Figure 5.12: Cumulative syndicate gross and net underwriting results, ordered from most to least profitable on a gross basis. The net underwriting results follow the gross in the same syndicate order. The difference in quantum between the lines is reinsurers’ share of the gross profit. SPAs have been excluded.

Figure 5.13: Distribution of syndicates’ annual gross U/W return (= 100% - Gross combined ratio) over time. Syndicates (dots) in the top left represent entities with high gross U/W returns and low volatility (good), syndicates (dots) in the bottom right have more volatile and lower gross U/W returns (bad). The vertical line represents the median.

Table 5.6: GWP, gross & net U/W result from Lloyd’s Aggregate Accounts, number of syndicates and top 5 share from individual non-life syndicate financial statements. Source: ICMR.Data

Financial year

Gross loss ratio

Gross expense ratio

Gross combined ratio

2015

38.1%

34.2%

72.4%

2016

54.5%

34.1%

88.6%

2017

103.8%

33.3%

137.1%

2018

75.3%

32.4%

107.7%

2019

57.4%

30.5%

87.9%

2020

73.8%

29.9%

103.6%

2021

55.6%

29.7%

85.3%

2022

62.1%

27.6%

89.7%

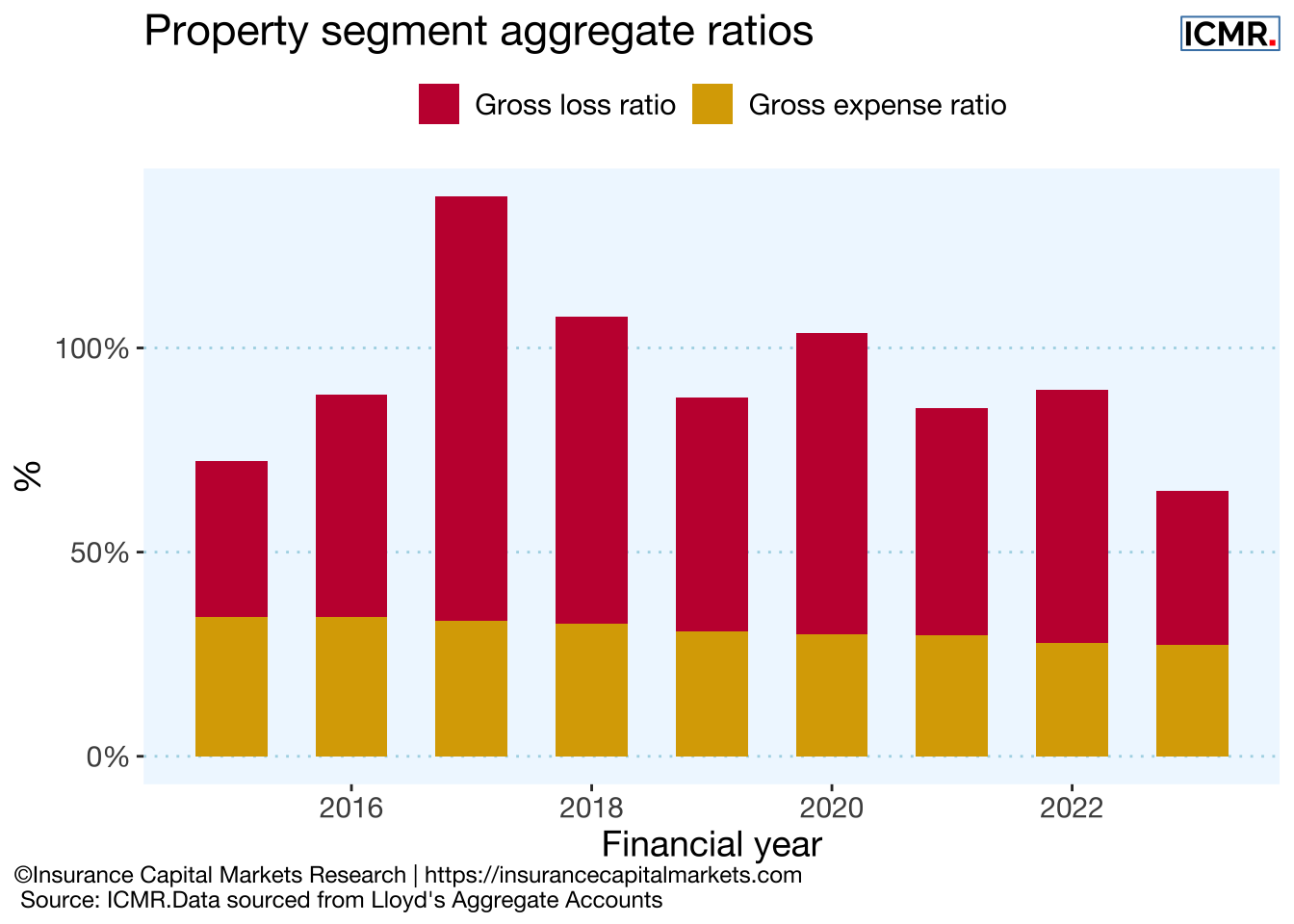

2023

37.6%

27.4%

65.0%

Mean

62.0%

31.0%

93.0%

StDev

20.5%

2.6%

21.2%

Table 5.7: ICMR.Data, sourced from Lloyd’s Aggregate Accounts

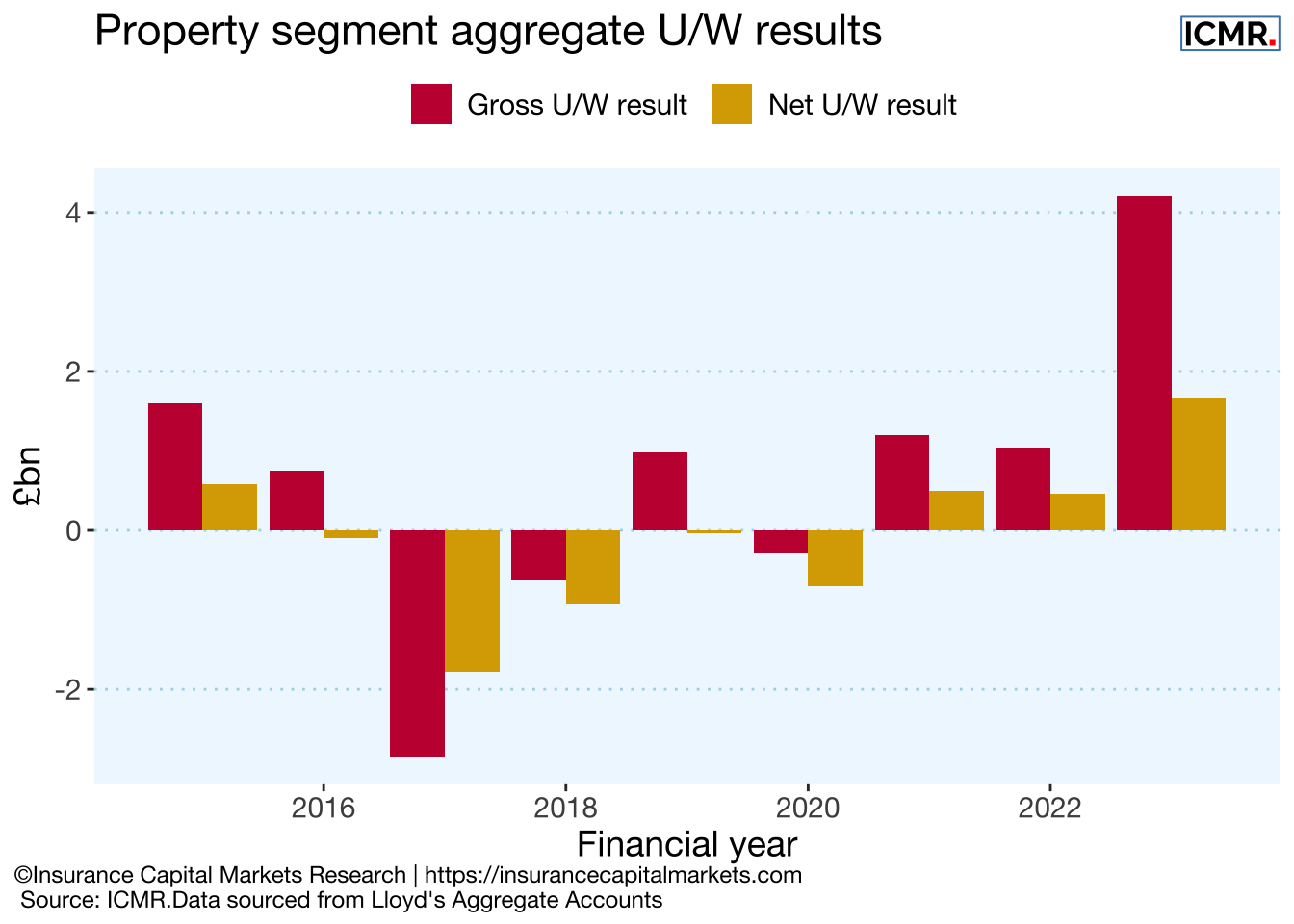

Figure 5.16: Cumulative syndicate gross and net underwriting results, ordered from most to least profitable on a gross basis. The net underwriting results follow the gross in the same syndicate order. The difference in quantum between the lines is reinsurers’ share of the gross profit. SPAs have been excluded.

Figure 5.17: Distribution of syndicates’ annual gross U/W return (= 100% - Gross combined ratio) over time. Syndicates (dots) in the top left represent entities with high gross U/W returns and low volatility (good), syndicates (dots) in the bottom right have more volatile and lower gross U/W returns (bad). The vertical line represents the median.

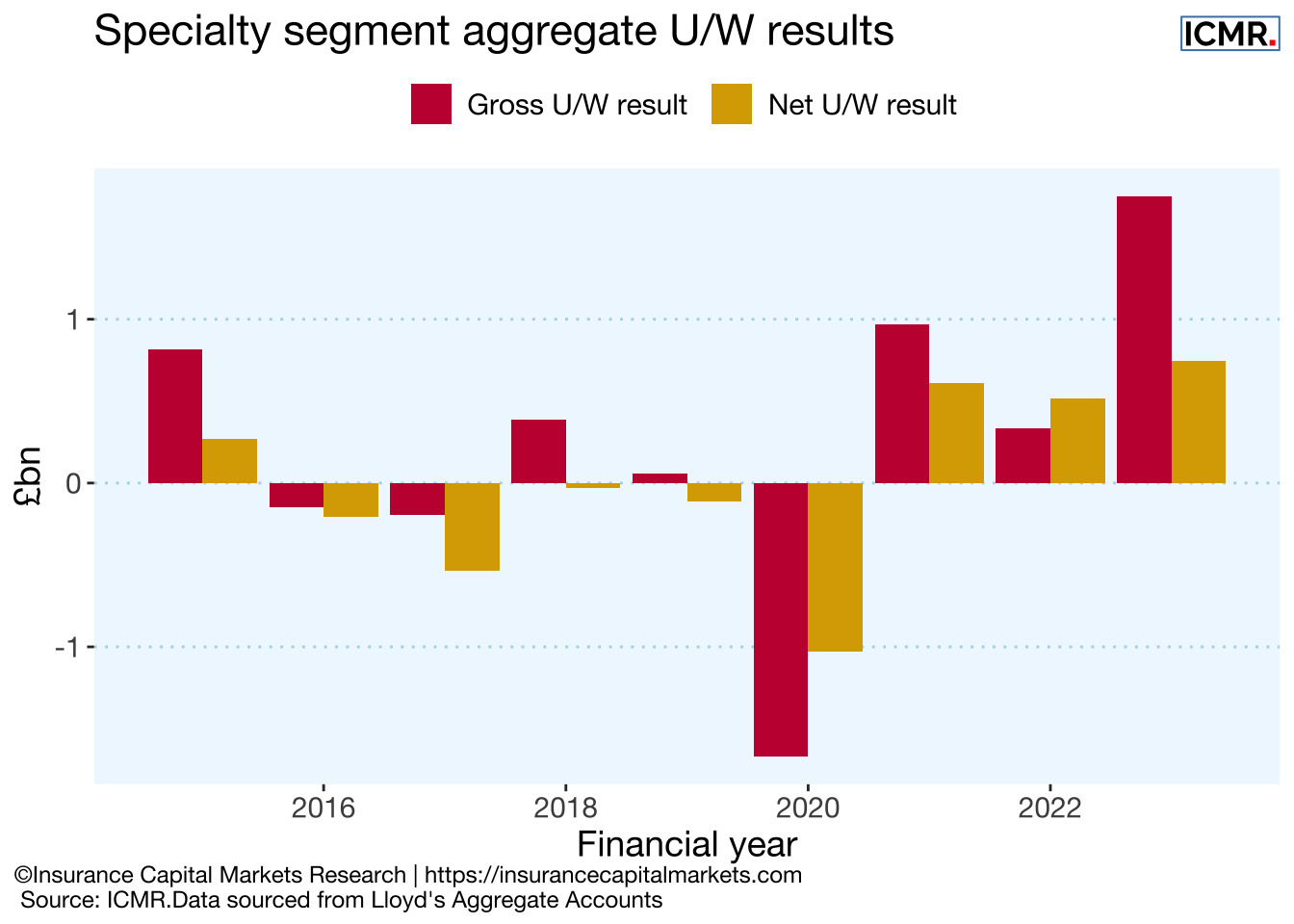

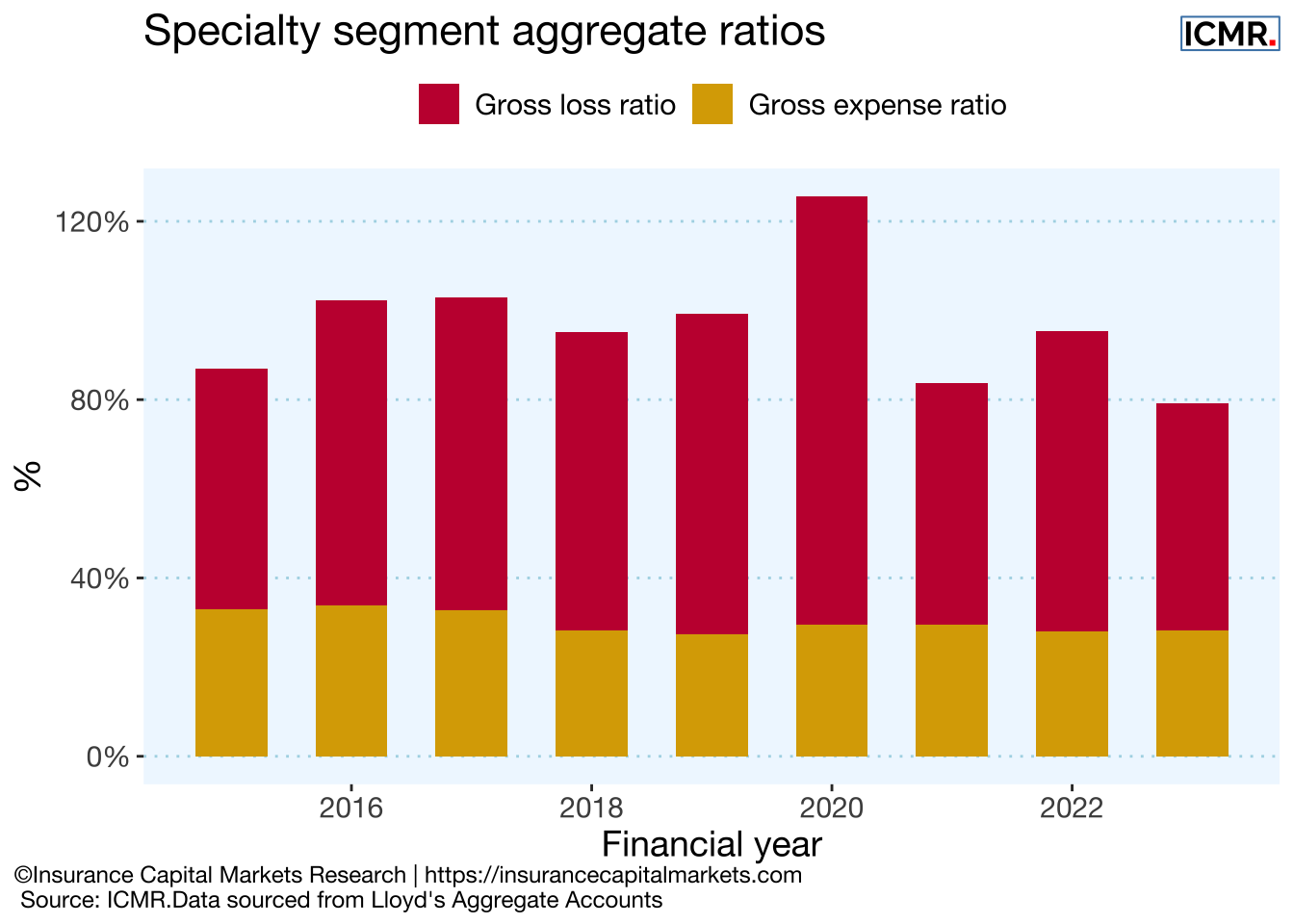

Table 5.8: GWP, gross & net U/W result from Lloyd’s Aggregate Accounts, number of syndicates and top 5 share from individual non-life syndicate financial statements. Source: ICMR.Data

Financial year

Gross loss ratio

Gross expense ratio

Gross combined ratio

2015

54.0%

32.9%

86.9%

2016

68.6%

33.8%

102.4%

2017

70.1%

32.8%

102.9%

2018

66.8%

28.3%

95.1%

2019

71.8%

27.4%

99.2%

2020

96.1%

29.5%

125.6%

2021

54.1%

29.6%

83.7%

2022

67.5%

27.9%

95.4%

2023

51.0%

28.2%

79.2%

Mean

66.7%

30.0%

96.7%

StDev

13.6%

2.4%

13.6%

Table 5.9: ICMR.Data, sourced from Lloyd’s Aggregate Accounts