Decoding Lloyd’s Returns: Third-party Capital and the True Cost of Syndicate Participation

As the market cycle shifts, proprietary ECA modelling reveals the real risks, rewards and hidden costs for third-party investors

The Dynamics of Unaligned Capital

Given we are now in the middle of June, syndicates have already begun their business planning for 2027. For investors, this makes it a critical time to review portfolios, considering potential tweaks and strategic shifts. However, navigating this requires timely data and intelligence.

In this article, drawing upon insights from our comprehensive ICMR Syndicate Statistics publication, we examine the dynamics of third-party capital and the true costs associated with participation.

In this article, drawing upon insights from our comprehensive ICMR Syndicate Statistics publication, we examine the dynamics of third-party capital and the true costs associated with participation.

Opportunities for private investors relate both to their “freehold” capacity ownership, complemented by emerging “leasehold” capacity opportunities particularly in new start up syndicates. Because investors must participate continuously to maintain their freehold capacity, they will likely relinquish leasehold capacity first when looking to downsize in a softening market.

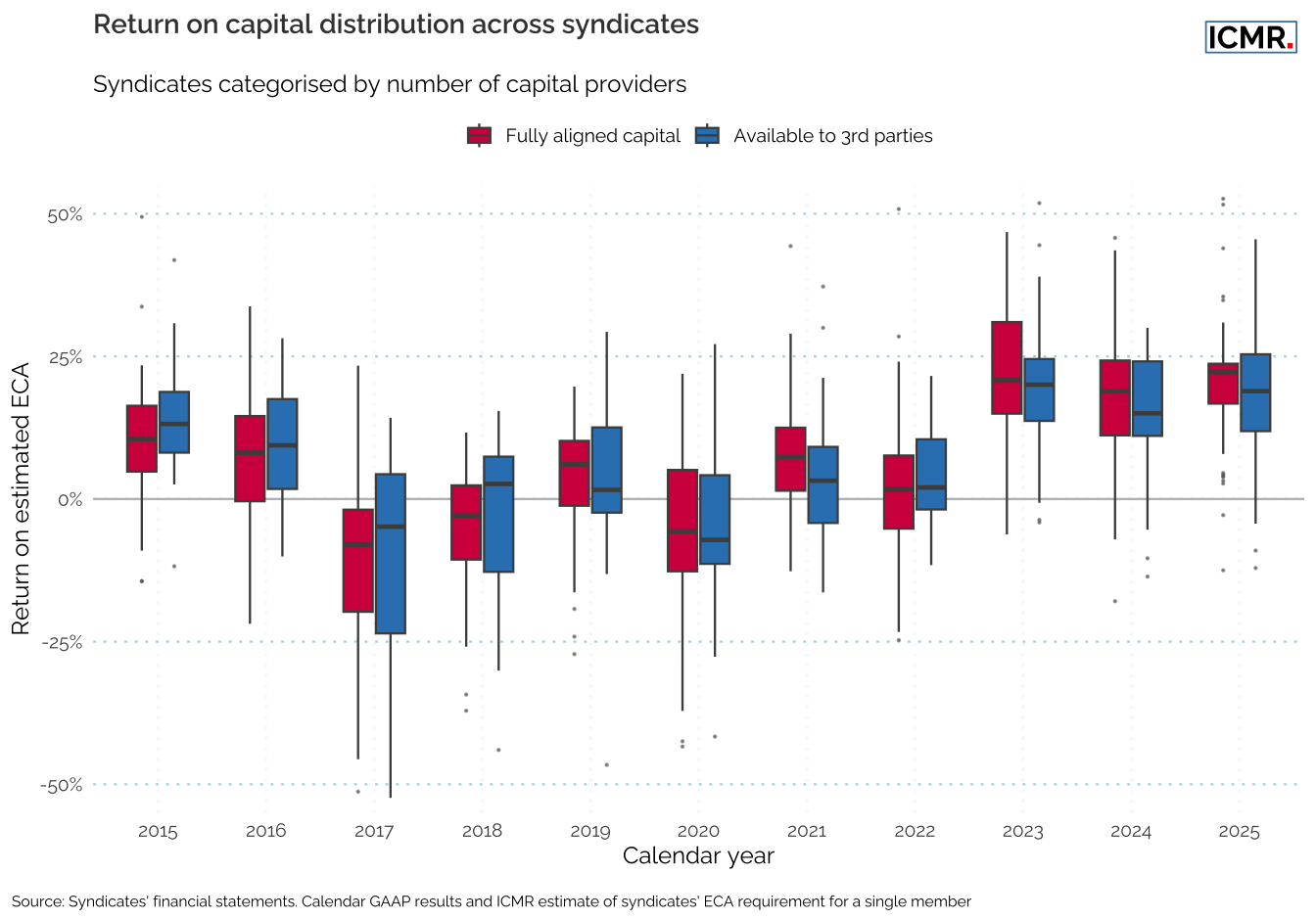

Our broader analysis of the market highlights a distinct range of return on capital outcomes when comparing fully aligned and unaligned syndicates, which accept third-party capital1.

Crucially, because syndicates’ Economic Capital Assessment (ECA) requirements are by and large not in the public domain, the returns on capital discussed here are based on ICMR’s proprietary estimates. Leveraging our ICMR.Quant framework enables us to model and estimate every syndicate’s underlying capital requirements, providing investors with an otherwise inaccessible view of true performance metrics.

Figure 1 illustrates the historical range of return on capital outcomes between these fully aligned and unaligned syndicates.

Both types of syndicate demonstrate a wide range of outcomes for potential investors. Throughout the last ten years, all ranges encompassed some negative returns, even during the recent hard market recovery—highlighting the critical importance of rigorous syndicate selection. However, a key observation is that median performance tends to be higher for aligned syndicates during hard market phases. This situation appears to reverse in softer market phases, with the median unaligned syndicate tending to outperform the median aligned syndicate.

In any market condition, an investor’s need for rigorous scrutiny of performance data—especially regarding modelled marginal capital requirements—is paramount.

Syndicate Access and the True Cost of Participation

For managed funds, investment opportunities remain most likely at the level of building portfolios of syndicates where such funds participate as third-party capital. Here, participation is structurally similar to private investors, with a key difference: such funds rarely acquire freehold capacity at auctions, partly due to the impact on the Internal Rate of Return (IRR).

Interest from this segment has grown significantly over the past 18 months, although deploying these funds is not always straightforward. It remains a market truism that the highest quality syndicates are consistently the most difficult to secure capacity allocations on.

One common thread in our work with various investor groups recently has been the critical importance of factoring in ALL costs associated with participation. These include:

- All fees payable (intermediary, managing agent, members’ agent, or fund manager).

- Any specific overriders and profit commissions attaching to participation on specific syndicates.

These costs can vary significantly from syndicate to syndicate. It is only by bringing all these items together in the investor cashflow that truly realistic investor IRRs can be calculated.

Seeing the full economics of participation alongside how it manifests through regular Net Asset Value (NAV) reports can help investors understand if their target IRRs are still achievable, or if pre-emptive adjustments are required. As Tom Bolt, the late former Performance Management Director at Lloyd’s, used to say:

“In insurance you can be on your third child before you know you are pregnant.”

Tom Bolt, former Performance Management Director at Lloyd’s

Equip Your Investment Strategy with ICMR

Navigating the complexities of Lloyd’s requires robust data and independent analysis. ICMR provides the tools necessary to isolate genuine outperformance from market noise and make informed capital allocation decisions.

- The 2026 Syndicate Statistics Book: Go beyond simple reporting with our comprehensive 272-page book. It provides a forensic analysis of every active Lloyd’s syndicate, condensing complex financial statements into highly digestible, two-page snapshots. Purchase your hard copy directly from the ICMR website.

- ICMR.Data & ICMR.Quant: The Syndicate Statistics book is the snapshot; ICMR.Data is the engine. Gain unique access to every Lloyd’s syndicate’s whole account and gross line of business underwriting performance in a single Excel workbook, and leverage our proprietary ability to model unpublished capital requirements.

- Regular NAV Reporting & Portfolio Review: Investors demand transparency. ICMR offers independent Regular NAV Reporting, incorporating real-time public information on major loss events. Leverage our unique experience and skills to review syndicate portfolios and access senior-level Lloyd’s expertise without the in-house headcount cost.

Contact ICMR today to discover how our quantitative insights can support your investment strategy at Lloyd’s.

Footnotes

Unaligned syndicates are those we believe are open to third-party capital on either freehold or leasehold bases, or both. Some syndicates that appear aligned may have third-party capital at the member level; public data does not consistently provide underlying capital structures.↩︎